Yougui Wang, Jinshan Wu, Zengru Di

1. Department of System Science at School of Management,

Beijing

Normal University, Beijing, 100875, P.R.China

2. Department of Physics, Simon Fraser University, Burnaby, B.C.

Canada, V5A 1S6

Abstract:

Econophysics is a new area developed recently by the cooperation

between economists, mathematicians and physicists. It's not a tool

to predict future prices of stocks and exchange rates. It applies

idea, method and models in Statistical Physics and Complexity to

analyze data from economical phenomena. In this talk, three

examples from three active main topics in Econophysics are

presented first. Then using these examples, we analyze the role of

Physics in Econophysics. Some comments and emphasis on Physics of

Econophysics are included.

Econophysics is a developing field in recent years. It's a subject

applying and proposing idea, method and models in Statistical

Physics and Complexity into analyzing data coming from economical

phenomena. Economics is a subject about human behavior related

with the management of the resources, finances, income, the

production and consumption of goods and services. So Economics is

usually regraded as a social science. But in some ways, the laws

in Economics are similar with natural science. Although it has to

deal with incentive and human decision, but sometimes the

collective behavior can be described by determinant process, at

least in a statistical way. So the aim of Econophysics is to apply

the idea of natural science as far as well into economics. Maybe

this will disentangle natural laws and human behaviors in

economical phenomena, and end with a new Economics.

Also because of the plenty data records of different systems in

our economy behavior, it's a treasure to physicists, especially to

the one being interested in Complex Systems, in which many

subsystems and many variables interact together. And the

development of Economics also provide many open questions, like

stock price, exchange rate and risk management, which may require

technics dealing with mass data and complex systems.

Physics tries to construct a picture of the movement of the whole

nature. Mechanism is the first topic cared by physicists. So

trying to describe and understand the phenomena is the first step

of econophysicists facing the mass data in economical phenomena.

Till now, we have to say, the most works in Econophysics are

empirical study of different phenomena to discover some universal

or special laws, and also some initial effort about models and

mechanism.

Therefor, in this talk, we will begin with three examples of

empirical works in Econophysics, and discuss very shortly about

the corresponding models and mechanism. Focus will be on the

Physics of Econophysics, to present the power of Physics to

Econophysics and some benefit which Physics will get from

Econophysics.

Recent works in Econophysics mainly in three objects. First one is

the time series of stock prices, exchange rates and prices of

goods. Size of firms, GDP, individual wealth and income are the

second topic, which can be regarded as wealth of different

communities. The third one is network analysis of economical

phenomena.

The prices of stocks are recorded every minute or every few second

everyday in stock market all over the world. The price of a stock

is driven by many factors, such as the whole economy environment,

achievement of enterprise, the prices of other stocks, and by the

buying or selling activity of stockholders. At the same time, the

behavior of stockholders is effected by the price, and further

more, everyone has his/her own decision which is different with

each other, but effected each other. So such phenomena seem

complex. While every enterprise has its own characters, and every

stockholder decide his/her behavior on his/her own knowledge,

information and belief, and every stock market has its own

environment, the empirical study shows some common stylized facts

valid for almost all stocks.

A typical time series of stock price, SP500 index, denoted as

, is showed in figure 1. Actually SP500 is a

stock index, which is a weighted mean value of stocks in a market,

can be used as a indicator of stock price. Some papers use the

data of indexes, some use individual stock, and also some paper

investigate all stocks in a market as an ensemble of stocks. In

this talk, we just use analysis of individual stock as examples.

Fig 1: Figures extracted from [5], time series of stock price. The first two figures at bottom are time series of return while the last one is a Gaussian noise

Because economy is in growth, so the time series of stock price

has a long term trend to increase. This means it's nonstationary.

So other than the original price, other quantities like different

and return may be better to use as analysis object. The difference

is defined as

(1)

in which is the time step to sample the time series. It

can be the time step of record, or a large time scale. Return is

defined as

(2)

It's equivalent with

when is small

enough.

Most works use return as object time series. The figures in the

lower part of figure 1 show examples of

, while

the last one is a Gaussian noise signal for comparison.

A statistical analysis of one time series can be classified as two

parts, the distribution properties which dismiss the time

information, and the autocorrelation analysis which mainly takes

time into account.

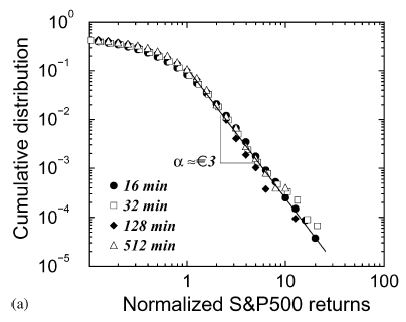

The frequency account of a data set formed by collecting all the

return values will give us the distribution, as shown in figure 2.

Fig 2: Figures extracted from [5], distribution of return. Log-normal for central part and power law heavy tail.

Detailed fitting shows the central part is a log-normal

distribution (

) while the tail is a power

law distribution (

). The more important

thing here is the universality. The distribution shape is

independent on the time scale (), and is a common

distribution for different stocks in different markets, even in

different countries. When an empirical statistical result is

universal, we have to ask for the common nature behind it.

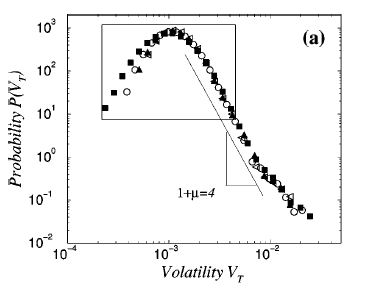

Another distribution properties is about the volatility of stock,

which is related with risk. So its characters is important for

risk management. Usually it's defined by local variation,

(3)

in which is a time window moving along with the

time, and is the mean value of

in

the window, as

(4)

In some papers, volatility is also defined as

(5)

in which absolute value is equivalent with square, and we don't

care about the mean value of , which can be set to be zero

when we analysis the distribution function or autocorrelation.

Also it was found that the distribution function is universal for

different stocks in different market during different time.

Similarly the center part is log-normal, while the tail is power

law, which is shown in figure 3.

Fig 3: Figures extracted from [9], distribution of volatility. Log-normal for central part and power law heavy tail.

Besides the distribution property, most information of time series

is included in time. Now we present the result of autocorrelation

analysis of return and volatility[5]. The

autocorrelation of a stationary time series is defined as

(6)

It can be investigated by spectrum analysis. But for a

nonstationary one, a recently developed detrend fluctuation

analysis (DFA)[35] is commonly used.

In figure 4, the autocorrelation functions of return and

volatility are plotted together. We can find an exponential drop

off in return with a time scale of minute, while a power law

decrease in volatility without a finite time scale. Think about

this phenomenon, a time series almost without an autocorrelation,

but a extremely high autocorrelation in absolute value, or local

variation. It's amazing. The fast dropping off guarantee the

validness of Efficient Market Hypothesis, while the long time

autocorrelation in volatility make it possible to construct a

theory of risk management. So such works will boost the

development of risk management, even a reformation.

Fig 4: Figures extracted from [9], autocorrelation of return and volatility. Exponential decay for return while power law decay for volatility.

All the analysis above looks like kinetics, which solve the

question how to describe the movement and what's the movement. The

next question in the tradition of Physics is how can such movement

happen. So next step, let's think about what are the factors

effect the stock price. And again, we may try to keep our eyes on

empirical study as far as we can. Demand and supply decide the

price is a central law in Economics. Although we know it's for

price of goods, maybe it will still be valid for stocks. So it

leads us to empirical study of order book of stocks, which study

the relation between difference of prices and the transaction

volume[16,17]. For a individual stock, they

recorded transaction volume as the total volume of every

transaction before the price changed, and define the difference of

the logarithm of the price now and price before such change as

price shift,

(7)

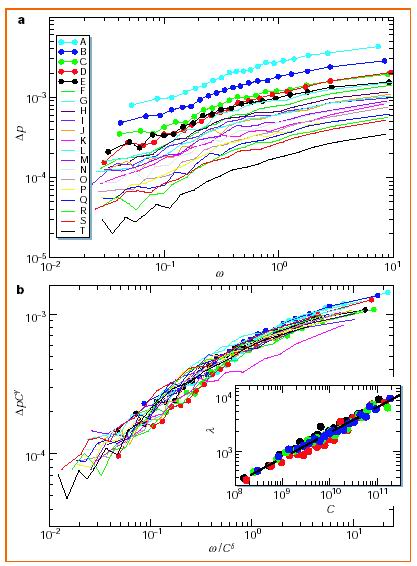

Then plots of price shift (

) vs

transaction volume (

) are presented in the

up part of figure 5. In the lower part, the authors found all

curves can be collapse onto a common line by rescale. So it's also

a universal law for all stocks.

Fig 5: Figures extracted from [16], A master curve for the relation between price and volume.

From the above results, it seems that stock price is only

determined by transaction volume. But it's sad to say, the

transaction volume is also decided by price. No direct way to

predict transaction volume. It should be decided together with

price by other predictable or known variables. So let's say if we

have only one stock, and the whole history of this stock is

already known, the achievement and activity of the enterprise is

also predictable by other ways, and so is the external economy

environment, at least in a statistical way, which means if they

are random variables we know the distribution and correlation, in

such condition, is the future of this stock determinant, and is it

predictable or chaotic? Or at least we can reproduce the similar

data with the same statistical characters as the empirical data?

If it's possible, what's the central variables, and how it can be

generalized into a stock ensemble, not only one stock?

The questions above ask for a mechanism model of stocks. Maybe

it's not very possible to reproduce the exact time series, but if

the stylized statistical facts are reproduced, the model is well

done in physical sense, although not in a sense of making money.

Let's check what's the central variable left after so many things

settled down by us including initial condition (even history),

boundary condition (only one stock), external variables

(enterprise and environment). So the only one thing left here is

how do stockholders buy and sell the stock under different price

and how does the price effected by the transaction.

The first idea here is activities of all stockholder are effected

each other. Such interaction maybe is indirectly through the price

and market, or by external way such as personal relationship. As a

tradition in Physics, a first approximation is treat every

stockholder independently, so they will only effected each other

through market. Like in spin model, every stockholder will has a

unit volume can buy or sell every time. Buying will improve the

price while selling lowers the price. Everyone is trying to make

more money in this game. So till now, a toy model has been

constructed for mechanism of stock price. When the detail of

benefit evaluation of every player and the effect on price by one

unit volume is set, this toy model will evolute in its own way, of

course when some specific behavior of all external variables are

also settled down.

Although it's only a toy model, we also can test some fundamental

knowledge, such as benefit and rational agent, and also try

different form of external variables. For example, we can take for

granted that external variables are random signals with fixed

distribution and without autocorrelation of any order. So our task

will be how can we construct our model to reproduce the

autocorrelation behavior in empirical study from no

autocorrelation input external data.

And then, if the output data is totally incomparable, maybe we

have to add something we dismissed, like the relation between

stocks. You know a phone call from your close friend may change

your decision. So it's very possible we have to take such

interaction into consideration. The model in [10], is

a representative one of such toy models. Although many different

interaction forms we can try, or even we can coevolute the

interaction strength together with the stock price, it's possible

that the output data is still incomparable with empirical one.

Then, we will have to include the interaction between different

stocks, and maybe further more a coevolution system including the

behavior of enterprises.

Oh, no, wait a minute, this is not on the way of physics now. More

and more variables, more and more subsystems, uglier and uglier

picture. It shouldn't. The Physics of Complex System tells us

maybe only a few ones rule the system. So the toy model maybe

imply something valuable. Now we come back to empirical study and

toy model, but in another way, the way keeping Physics in mind.

Not only the stocks, also exchange rates, goods and options are

under analysis nowadays. However, the universal results for stocks

seems not valid for other goods and options. The empirical study

of land price[31] gives the high skew and heavy tail

distribution of price (

) and power law

distribution for relative price

(

. And

empirical study of return of options shows unsymmetrical power law

distribution[33].

And not only the prices, waiting time can also be take into

consideration. In a real stock market, transactions do not always

happen in every minute or every half minute. It's also a random

variable. And the prices change depending on the transactions.

This is the so-called continuant time stochastic process.

Empirical and model analysis just started

up[11,12,13].

Interaction between different communities such as trade,

cooperation and competition, plays important roles in economy. As

a result of such activities, the wealth distribution carries some

valuable information for researchers to investigate the properties

of such interaction. So the second active main topic in

Econophysics is about the size distribution. For a firm, size can

be measured by employee, sales or capitals, while GDP for a

country, income or wealth for a person.

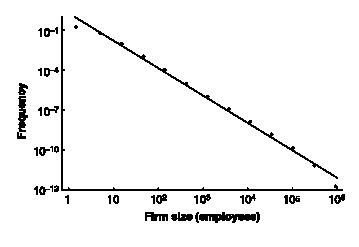

In [22], the author collected data including more

firms especially small firms in a longer history than the database

in [21], so the result of power law distribution seems more

convincing than the log-normal distribution in the later. And the

important character about such distribution is the universality.

Different measurement of size such as total employees, sales,

assets and capitals give the same distribution. And it doesn't

depend on the time, even during the years of significant change of

working force. Further investigation[24] shows

it's also a common law in different countries. A typical

distribution is shown in figure 6.

Fig 6: Figures extracted from [22] and [27], Zipf plot of sizes of firm, and Zipf plot of size of GDP of countries, nearly a perfect power law.

Similar results have been get for GDP of countries all over the

world. Power law distribution of GDP per capita of different

counties has been revealed in [27].

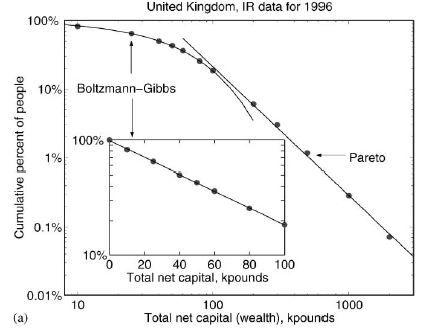

For individual such distribution can be analyzed by personal

income or wealth. A typical result[29,30] is shown

in figure 7. The lower income seems like exponential distribution

while the higher part is power law. From experience of ideal gas,

we know, the equilibrium energy distribution of a random exchange

system is exponential. So maybe in the lower income community, the

cooperation and competition between individuals is in a way

similar with random exchange. But for the higher income part,

different interaction like preferential attachment part more

important role.

Fig 7: Figures extracted from [29], Cumulative Distribution Function of individual income and wealth.

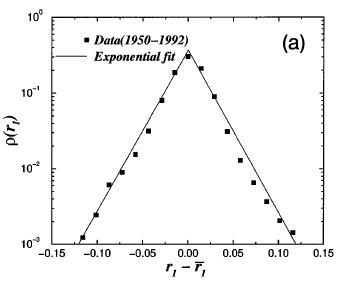

Growth rate of firm size is defined similarly with return as

(8)

Then in an ensemble of firms, every firm has its own track, and at

every time, we have a cross-section data set including all firms.

In a tradition of Statistical Physics, analysis can be done along

two ways, keeping eyes on individual time series or just dealing

with cross-section data. In an ensemble consist of identical

systems, those two ways will give the same result. However,

although here we can make an assumption that all firms act in a

common way, which is the way we want to find, our ensemble is not

consist of identical systems. So the compromise here was to treat

the firms with the same size as identical systems, and to dismiss

the time information and mix them together.

At last, we will have conditional distribution function for

different size as

, where is the

initial form size. Actually, such analysis is on the first way we

mentioned, keeping eyes on fixed firm, so we get

, where is the label of firm. But

here, a little further we go, the tracks starting at the same size

are combined together. The distribution of growth rate is shown in

figure 8 as Laplace distribution,

Fig 8: Figures extracted from [26] and [28], Distribution of growth rate of GDP.

(9)

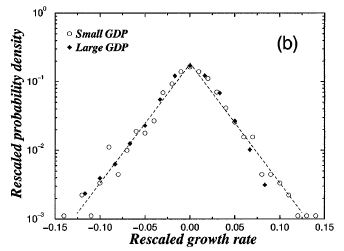

Similar growth rate analysis has also been done for GDP. The gross

growth rate of GDP is defined as

(10)

But since the long term growth trend of economy, when we want to

analysis the fluctuation information, such endogenous unknown

trend has to been excluded. In [28], the author suggested

to use a decomposition as below,

(11)

where is the long term expected endogenous growth

rate,

is a common fluctuation to all

counties, and

is the residual which

represents fluctuation, the one we want to investigate. As shown in Fig 8-(b), it has

the same Laplace distribution.

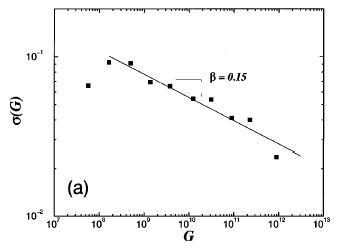

From experience in Statistical Physics, relation between

fluctuation and size usually gives important information of the

underlying processes[26]. Like in idea gas with

independent particles, the magnitude of fluctuation is invert of

the square root of the system size as

(12)

Corresponding analysis can be done for growth rate of firm size

and GDP. A power law relation but with exponent other than

has been revealed by

researchers[26,28], as shown in figure 10. And further more, such

exponents is universal for different measurement of firm size,

independent on time and locations, and the values for firm size

and GDP is very close. So maybe this implies some common mechanism

for firms and GDPs.

Fig 8: Figures extracted from [26] and [28], Relation between variation and size.

Economy is a many-body system including agents as individuals,

firms, countries, goods as produce, production and service, and

subsystems as financial system, manufacturing, agriculture,

service industry. And all of them interact with each other. A

general way developed recently to describe such system is Complex

Networks. In a complex network, every agent is represented by a

vertex and the interaction between any two agents is described by

a link between the two corresponding vertexes. Further more, the

weight of links can be used as the strength of the interaction and

a directed link can be used when the interaction is not

symmetrical.

A recent such development is the web of

trade[14,15], in which vertexes are the

countries and links are the inport/outport relation. The basic

structure and efficiency has been analyzed, like high clustering

coefficient, scale-free degree distribution.

Another widely used network of economy system is the interaction

between stock agents. Every stockholder is a vertex in the

network, and the effect from decision of one agent to another is a

directed link from the former vertex to the later. So the network

acts as a whole system to drive the stock price. The geometrical

character of such network will have some important effects on the

dynamical behavior of stock price. Therefor, such investigation

maybe will reveal the interaction pattern between stock agents.

The third proposed works about network of economy systems is the

network analysis of product input/output table. Like the

Predator-Prey Relationships in food web, every product made from

other products or raw materials, and also become input of other

products. So the input/output relationship between products forms

a network. Actually the input/output table analysis in Economics

has the same spirit but in a highly clustered level and asking for

different questions. So, although a database of product relation

is what we need, a clustered group product relation data set will

also be able to be used here as an beginning analysis of basic

structure characters. And further works will require detailed data

on input/output relation of products.

Construction and analysis of such clustered product network is in

progress[36]. Characters on degree distribution,

clustering coefficient, weight and weight distribution, average

shortest distance have been gotten, but questions about the

universality of such properties need to be tested on more

networks. The links between products can be regarded as

technology. So a score analysis such as link betweenness will show

the relative importance of different technics, therefor it may

imply some new direction of development of technology. Further

questions about the robustness of such networks can be asked as

how many total product will be lost if one or several

inter-products were in shortage, or when the resource distribution

was changed, or as how many total product will be lost when one or

several link (technics) were dismissed, or inversely, if a new

link was invented how many product will grow in total. Such

investigation will relate traditional questions in economics such

as resource allocation, social welfare, and effect of new

technology with network analysis of product. It can have a

far-reaching effect both on economics and network analysis.

We took a review of Econophysics including empirical study and

models on three topics above. Now we try to discuss the question

why is Econophysics? Since dynamics of Stock price is also a topic

of Mathematical financial, what's the difference between this and

Econophysics? If Physics provide insightful tools for this new

field, can Physics also benefit from it?

First, let's discuss the role of Physics as tools in Econophysics,

the application of concepts, models and method developed in

Physics into Econophysics.

There is many-years experience to deal with many-body system and

complex system in Physics. The concepts and technics such as

ensemble statistics, correlation and self-correlation analysis,

have been widely used to reveal the property of economy phenomena.

And the more important thing here is experience in Physics helps

to understand what the properties imply. For instance, a power law

is usually related with critical phenomena in Physics, including

critical point of equilibrium and non-equilibrium phase

transition. And so does a long range order and a high

self-correlation. Also as pointed in [26], relation

between variation and size imply the form of interaction.

Another central analysis method transplanted from Physics is Data

Collapse and Universality. If relation curves from different

systems can be collapsed onto a master curve by scaling, it's very

possible to find some common mechanism from such systems. And if

an empirical or theoretical relation is independent on time

period, some different detail of objects, it's called

universality. When a universal law is found for different systems,

the systems must be equivalent in some ways. So it implies common

mechanism and others can be understood if we know one of them very

well. Therefor, it open a new way to investigate such systems,

especially when some models with similar properties in Physics and

other fields can be used here as a reference model for economy

phenomena.

Spin model is widely used to describe human decision in stock

market[] or other economy activity[].

Usually, status of an agent can be one of

,

which is interpreted as buying, waiting and selling, or one of

. So the status space of the whole system

with agents is

.

The benefit of every agent is determined by a payoff function

, in which are the

interaction constants of all orders and are the internal

variables as stock price, or external information like environment

and behavior of enterprise. Everyone intend to maximize its own

benefit in a statistical way[,] like

(13)

in which is an average evaluation coefficient, which means the

effect on ones decision for a unit benefit. Actually such form of

human decision comes from the ensemble distribution in Statistical

Mechanics. In metropolis simulation of a spin system, the

probability for a spin to transfer its status is overruled by a

similar form. An ensemble distribution here means in statistical

way, in a many body system, although everyone try to stay on

maximum position, but the end status is much like an ensemble

distribution.

Such application gives some reasonable results, although it may be

not totally equivalent with assumption in Economics, where every

agent must stay on its maximum point, not a distribution function.

In Mechanics, the status of physical object is determined by

Newton's equations or minimum action principle, but for a

many-body system in Statistical Mechanics, ensemble distribution

is used instead. Although it's not deduced from first principle,

it works widely. Maybe similar approach can be developed in

Economics.

Ideal gas is another reference model widely used in

Econophysics[]. In a first order approximation model of

competition and cooperation between firms, or between individuals,

every agent can be regarded as random exchange wealth with each

other, like random exchange energy in ideal gas. So the

equilibrium distribution will take the exponential form. It's

amazing that the central part of personal wealth is actually

exponential form. Further possible model can be generalized random

interaction model, including not random exchange, but also random

increase or decrease process, or extended model with bias exchange

model, like preferential exchange, in which rich one has higher

probability to get richer.

In above section, we discussed the role of Physics in

Econophysics. In this section, we ask for the inverse question,

what Physics can benefit from Econophysics, not only as an

insightful tool.

Frankly, physicists are kinda aggressive, so is Physics. When a

question asking for reason of a phenomenon in a common sense, or

in a fundamental way, according to physicists it's a physical

question. Econophysics is such an example. It choose the special

phenomena from Economics, and ask for the reason, or mechanism in

physical language. Most phenomena concerned in Econophysics

exhibit universality independent on time period, detail of

systems, and even different economical structure of countries. So

such question is likely very much to ask the behavior of a system

with known interactions, or the interaction form of a system with

known behaviors. It's a typical physical question.

Like DFA method proposed by researchers in Statistical Physics

from works in DNA sequence and physiologic signals, new technics

can also be invented from Econophysics. Hopefully, not only

technics, but also concepts and fundamental approach may also be

proposed.

For instance, effect of geometrical property such as dimension and

curvature on dynamical behavior is an important question in

Physics. Actually it's widely studied in Physics including

Relativity, Quantum Physics and especially Phase Transition and

Critical Phenomena. So if geometrical quantities can be defined in

Complex System, and the effect on dynamical process is known, it

will partially predictable just through grasping the geometrical

properties of such systems. For example, in principle, the

make-from relationship between all products is tractable. So the

network can be explicitly constructed, and even part of the

history is known, like the things changed when reformation of

technics happened. So Economics provide some nearly perfect

treasure for Physics. And further more, the special character of

such network will definitely require new quantities or technics to

describe the effect. This will maybe boost the development of

Physics.

Not all human behaviors are rational or determinant, like

impulsion and inspiration, but some of them, are determined by

environment at least in a statistical way. Personal character

affects human decision. But if all other factors could be

determined by physical way like a dynamical equation, and the

statistical properties of personal characters of the system were

known, it will be easy to predict the behavior of the system. So

the most valuable question left here is that whether we can

describe economy system and human behavior by physical way as far

as possible and leave something unknowable in physical sense. If

it's possible, how to do it. I think, Econophysics is a good try

in such sense.

Economics is a science of human behavior, but it's fortunate that

Economics is not totally a science of human creativity and

inspiration like fine art. This means that some part, even most

part according mathematicians working in Economics, of Economics

can be modelled in an abstract or mathematical form. It's

interesting to point out that it's Physics the most famous

masterpiece applying Mathematics into nature, not any other field

of Applied Mathematics. So it's natural to incorporate Physics

into Economics like to imitate masterpieces.

And through such exploration, it's possible that Physics will be

widely used in social science. This will greatly extend the scope

of Physics, and maybe will help Physics to deal with some hard

topic such as turbulence, or more general complex systems.

At lease, Econophysics provides, invents and develops tools for

analysis of Economy phenomena, and investigation of economy system

generalizes the scope of Physics. But will Econophysics effect

concepts and thought in Physics? It depends on the future.

However, we are sure that both Economics and Physics can benefit

from such exploration. Therefor, as a researcher in physics in the

new century, or a potential economist, should we learn from each

other?

Thanks is given to Fukang Fang and Zhanru Yang for their

simulating discussion. And we own graduate students 2002 in System

Science Department for their warm discussion and good questions.

The author Wu want to give thanks to Qian Feng for her

encouragement and understanding. This work is partial supported by

National Natural Science Foundation of China under the Grant No.

70371072 and No. 70371073.

R. N. Mantegna and H. E. Stanley, An Introduction to Econophysics:

Correlations and Complexity in Finance (Cambridge University Press, Cambridge, England, 1999).

H.E. Stanley, P. Gopikrishnan, V. Plerou, L.A.N. Amaral, Quantifying uctuations in economic systems by adapting methods of statistical physics, Physica A 287, 339-361(2000).

P. Gopikrishman, V. Plerou, Y.liu, L.A.N. Amaral, X. Gabaix and H.E. Stanley, Scaling and correlation in financial time series, Physica A 287, 362-373(2000)

V. Plerou, P. Gopikrishman, L.A.N. Amaral, M. Meyer and H.E. Stanley, Scaling of the distribution of financial market indices, Phys. Rev. E 60, 5305-5316(1999).

V. Plerou, P. Gopikrishman, L.A.N. Amaral, M. Meyer and H.E. Stanley, Scaling of the price fluctuations of the individual companies, Phys. Rev. E 60, 6519-6529(1999).

Y. Liu, P. Gopikrishman, P. Cizeau, M. Meyer, C. Peng and H.E. Stanley, Statistical properties of the volatility of price fluctuations, Phys. Rev. E 60, 1390-1400(1999).

A. Krawiecki, J.A. Holyst and D. Helbing, Volatility clustering and scaling for financial time series due to attactor bublling, Phys. Rev. Lett. 89, 158701 (2002).

M. Raberto, R. Gorenflo, F. Mainardi, E. Scalas, Scaling of the waiting-time distribution in tick-by-tick financial data (Poster presented during the international workshop Economics Dynamics from the Physics Point of View held in Bad Honnef (Germany) on March 2000).

M. Stanley, S. Buldyrev, S. Havlin, R. Mantegna, M. Salinger, H.E. Stanley, Zipf Plot and the Size Distribution of Firms. Economics Letters 49, 453-457.

L.A.N. Amaral, S.V. Buldyrev, H. Leschhorn, P. Maass, M. A. Salinger, H.E. Stanley and M.H.R. Stanley, Scaling bahavior in Economics: I. empirical results for company, J. Phys. I France 7, 621-633(1997).

L.A.N. Amaral, S.V. Buldyrev, S. Havlin, M.A. Salinger and H.E. Stanley, Power law scaling for a system interacting units with complex internal structure, Phys. Rev. Lett 80, 1385-1388(1998).

Y. Lee, L.A.N. Amaral, D. Canning, M. Meyer, and H.E. Stanley, Universal Features in the Growth Dynamics of Complex Organizations, Phys. Rev. Lett. 81, 3275(1998).

Di Guilmi, Corrado, Edoardo Gaffeo, and Mauro Gallegati, Power Law Scaling in the World Income Distribution, Economics Bulletin, Vol. 15, No. 6 pp. 1-7(2003).

A.A. Dragulescu and V.M. Yahovenko, Exponential and power-law probability distributions of wealth and income in the United Kingdom and The Unite States, Physica A 299, 213-221(2001).

G. Bonanno, G. Caldarelli, F. Lillo, and R.N. Mantegna,Topology of correlation based minimal spanning trees in real and model markets, arXiv:cond-mat/0211546 (2002).

The translation was initiated by Jinshan Wu on 2004-01-01

This is a review paper with some new idea included for further usage for Di's group at BNU.

Anyone who is interested in such works can contact with Prof. Di by zdi@bnu.edu.cn